Introduction

Current Situation of Shipping Industry in Vietnam

2.1. Shipping Companies

1) Vinalines

2) SBIC

3) Petro-Vietnamand Petrolimex

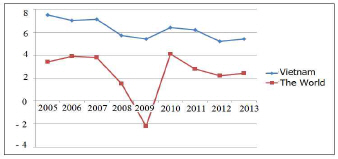

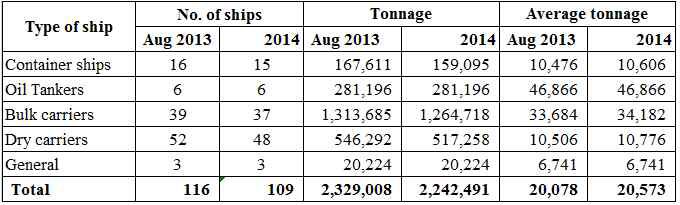

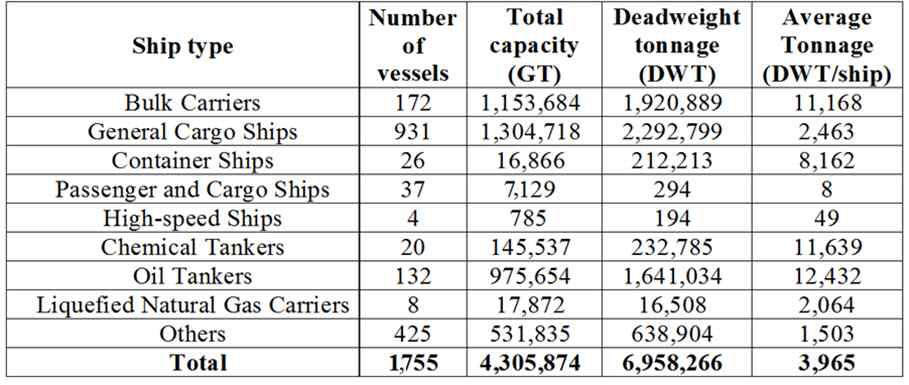

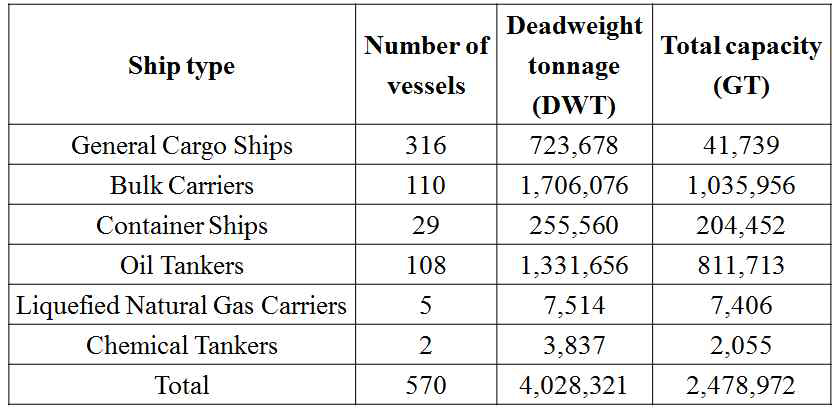

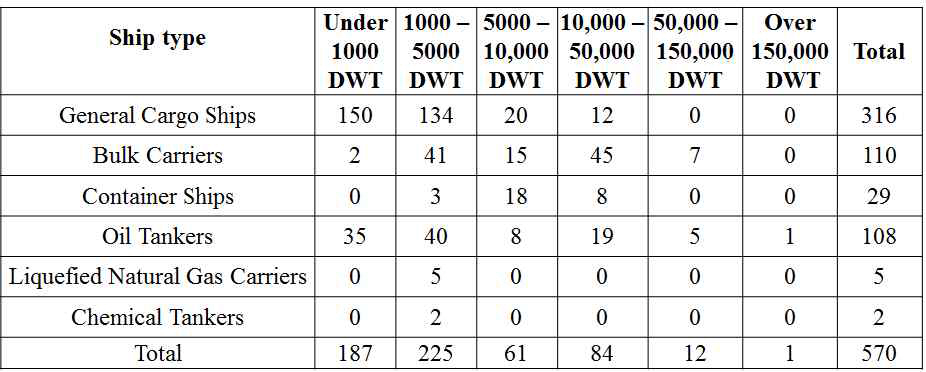

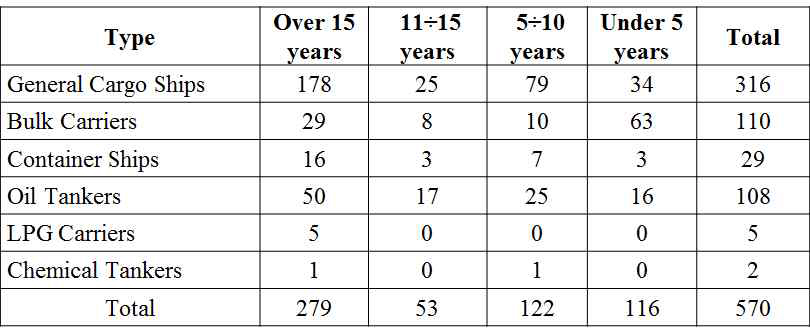

2.2. Tonnage of Vietnamese fleet

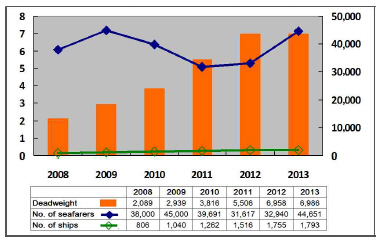

2.3. Seafarers

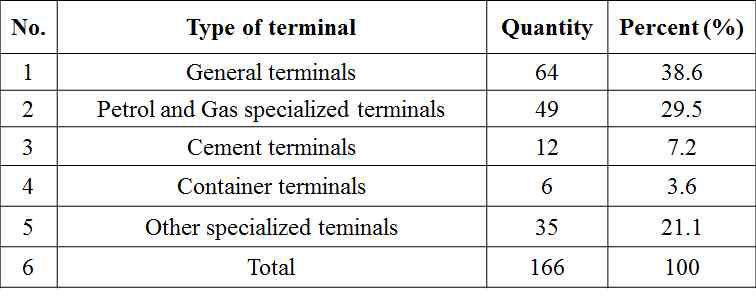

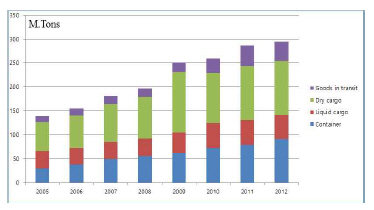

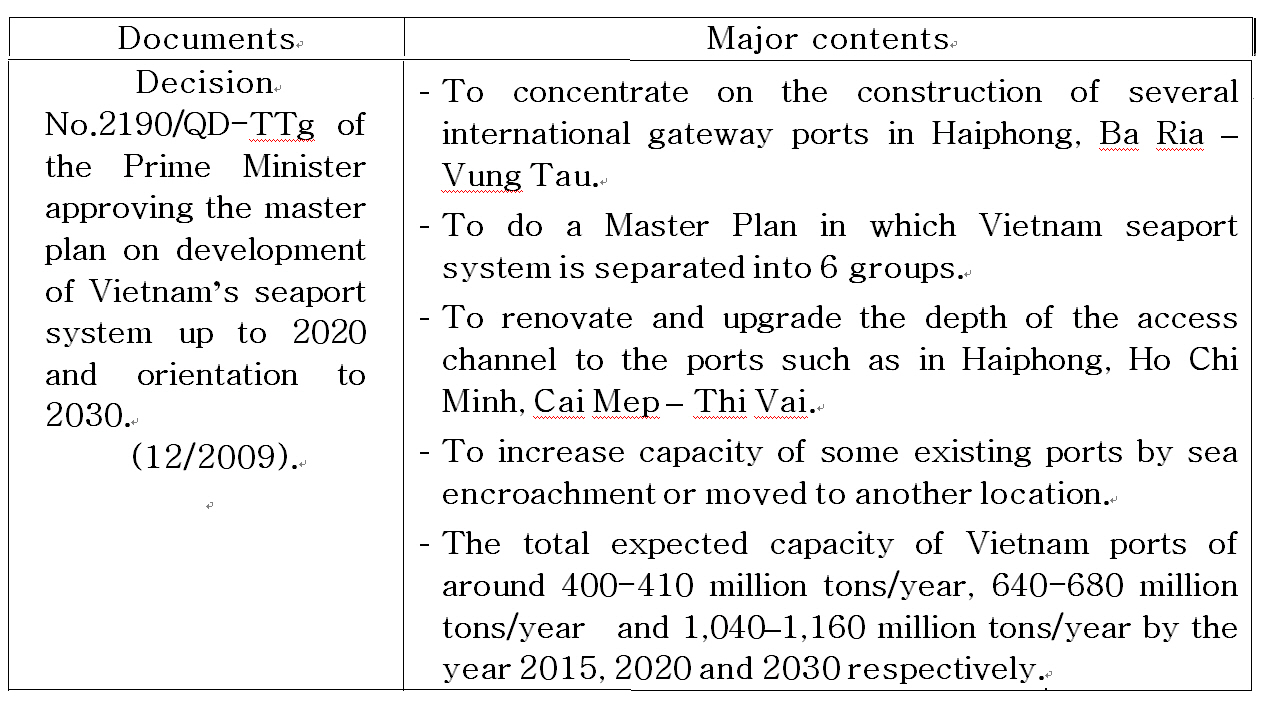

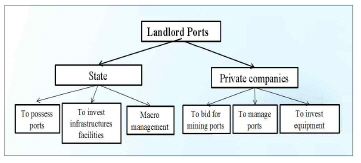

2.4. Ports

Policies on Shipping Industry and Outcomes of Implementation

To cut freight rates through reducing component costs, namely fuel, port and storage costs. The government now applies a preferential fuel price for Vietnamese shipping companies. In some terminals, such as in CaiMep terminal, all ships under 50,000 DWT have been discounted 45-50% of their tonnage cost. In addition, the construction of logistics centers and multimodal terminals, the investment of modern equipment with high capacity in ports, the acceleration of the application of information technologies like e-port authorities, e- customs, the implementation of a one-stop shop mechanism is also considered as a very good solution for reducing the above costs (VMA website, May 2014).

To renovate training methods and standards for the shipping workforce (Vietnam Ministry of Transport's website, 2014). To be more specific, maritime training centers have tried to raise the standard required to graduate , and now an English degree is considered as a prerequisite condition to apply the new educational method of training under the "requests" of the shipping companies (Vietnam Transport Ministry's website 2004).

To support the domestic shipping companies to overcome the consequences of the economic crisis through maintaining cabotage (Thanh-nien-online website, 2013).

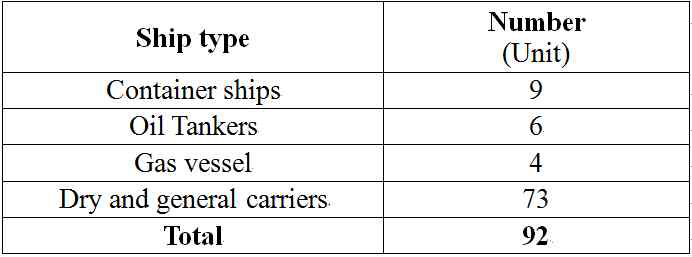

To reduce the operating cost of ships and to increase partial investment capital in new ships through fleet restructuring from 2011 to 2015. The number of ships that has planned to be sold or liquidated under the above guideline is estimated at over 40% of the total tonnage (in which approximately 1.4 million DWT has been planned for liquidation from 2011 to 2015 by Vinalines). The remaining fleets of Vietnam will be only about 2.5 million DWT by 2015 (VMA, June 2013, pp.25-26).

Summary and Proposal

The government may consider passing a short-term act which allows no penalties for the late payment of tax by shipping companies in order to accomodate these stake-holders that are overcoming overlapped losses after the crisis and backlog of tax.

Besides the Vietnamese shipping companies which possess small old ships, they in fact, have no competitive advantage in terms of price and quality of services when compared with other foreign shipping companies. Therefore, a Vietnamese fleet with new big vessels may need to be established as soon as possible. However, while the purchase of ships requires intensive capital, Vietnamese shipping companies in are in fact faced with a lack of money. Although they could use bank loans to buy ships, the interest rates in Vietnamese banks, as of May 2014, are at high level of 6.5% which is higher than that of other developing countries such as China (5.6%), Malaysia (3%) or Thailand (2%) (Trading Economic, 2014). It is obvious that borrowing bank loans is not a good way for them to acquire capital at this time. So, is it reasonable and necessary for the government to consider cutting the short-term lending interest rate? By doing so, it may make it easier to for Vietnamese shipping companies to acquire new ships via bank loans. Futhermore, it may help to attract more domestic and foreign investment capital into the shipping industry.

- In case of bulk cargo (coal and ore), a majority of coal and ore used in electrical and metallurgical industries in Vietnam are imported (estimated at 86-93 million tons by 2020). Bulk carriers with at least100-200 thousand tons of deadweight are considered as an economic option for bulk cargo transportation. These ships have not appeared in the Vietnamese fleet. Moreover, almost all of the electrical and metallurgical plants in Vietnam are invested in by foreign investors who will select their own transport contractors (FDI projects). Vietnamese ship-owners can win market share only if they have a competitive advantage on freight rate and service quality. Actually, this possibility becomes hard to realize in 5-10 years, because with each step up in ship size, the freight rate decreases (economics of scale) and vice versa. Therefore, in near future, the market share of the Vietnamese fleet should rely on coastal routes with smaller volumes which mainly cater for domestic consumption.

- In case of liquid cargo, Refinery Petrochemical Complexes in Vietnam are mainly joint ventures between Vietnam (with equity less than 30%) and foreign investors or 100% foreign-owned enterprises. Crude oil in use is mainly imported from Middle East, Africa and South America. So, like bulk carriers, the transport services of Vietnamese tankers mostly provide a domestic service.

- In the case of general cargoes and containers, containerization dominates more and more in shipping industry of Vietnam. Leading container lines around the world have been modernizing their fleets in an effort to reduce costs, raise service quality and carrying capacity, forming receiving/delivering nodes (terminals) styled on a ŌĆśMayer_spokeŌĆÖ model to attract cargo on axis East Asia-Europe-North America. As a result, it is very difficult for the Vietnamese fleet to compete on long-distance maritime routes (Europe, America) and average-distance maritime routes (Africa, Middle East, India, North East Asia). This is especially true in a period of cargo shortage and ship surplus in Vietnam currently, as well as in the next few years. Even on domestic routes, competitive pressures from large shipping companies in consolidation with containers for export and import at seaports also may affect the market share of the Vietnamese fleet. To deal with this matter, a more reasonable shipping schedule and more investment should be implemented as soon as possible.

PDF Links

PDF Links PubReader

PubReader Full text via DOI

Full text via DOI Download Citation

Download Citation Print

Print