An Empirical Analysis for Determinants of Secondhand Ship Prices of Bulk Carriers and Oil Tankers

Article information

Abstract

The aim of this study was to examine determinants of secondhand Bulk carrier and Oil tanker prices. This study compiled S& P transaction data taken from the Clarksons Research during January 2018 to April 2022 to see how independent variables influenced secondhand ship prices. In the secondhand ship pricing model of entire segments, size, age, and LIBOR showed significant effects on prices. A vessel built in Japan and Korea was traded at a higher price than a vessel built in other countries. In the bulk segment, size, age, Clarksea index, LIBOR, and inflation were meaningful variables. In the Tanker segment, unlike Bulk carrier, only size and age were useful variables. This study performed regression analyses for various sizes of Bulk carriers and Oil tankers. It verified that impacts of variables other than ship size and age were significantly associated with ship type and size while macroeconomic variables had no influence except for bulk carriers. By applying diverse variables affecting secondhand ship price estimation according to various sizes of Bulk carriers and Oil tankers, this study will expand the scope of practical application for investors. It also reaffirms prior research findings that the secondhand ship market is primarily market-driven.

1. Introduction

The shipping markets are historically known as highly volatile and risky market fluctuating its condition cyclically and repeatedly over the crest and trough(Haralambides et al., 2005). Stopford(2009) categorizes shipping markets as freight market, S&P market, new construction market and demolition market. Although these four markets transact different type of commodity, they are closely interacted with each other by the cause-and-effect relations. If freight rate increase, an investor will be interested in the market where they wish to participate by means of purchasing a secondhand ship from existing shipowner or build a new ship at a new construction shipyard. Contrarily, if the supply of world fleet exceeds than the demand of seaborne trade, the market will react reversely. Although the general market theory that markets are the simple mechanism that determine optimal volumes and prices based on demand and supply theory is also applicable for shipping market, external influences and boundaries, timing effects and disturbances make it really complicated(Kavussanos and Visvikis, 2016).

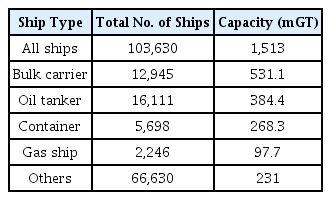

The supply side of shipping market is observed that the world merchant vessels(≥ 100 GT) comprise about 103,630 vessels corresponding total about 1,513 million GT in July 2022(Clarksons Research, 2022). The Bulk carrier segment transporting the major bulks for coal, iron ore and grain cargo, and minor bulks such as steel products, sugar, wood chips and cement cargo comprises 12,945 vessels which representing of total 531.1 million GT. The Bulk carrier is generally sub-segmented with Handysize, Handymax, Supramax, Panamax, Capesize and VLOC(Very Large Ore Carrier). The Tanker segment comprises 16,111 vessels corresponding 384.4 million GT. The Panamax, Aframax, Suezmax, VLCC(Very Large Crude Oil Carrier) and ULCC(Ultra Large Crude Oil Carrier) are the ships transporting the crude oil, and MR(Medium Range), LR I(Long Range I) and LR II(Long Range II) tankers providing coated cargo tanks are suitable to carry product oil and chemicals. Remained segments of commercial ships are Containers, LNG carriers, Gas ships, PCTC(Pure Car and Truck Carrier), Passenger ships and various types of miscellaneous ships specializing for carrying cargo and passengers. Table 1 summarize the volume of main shipping segments.

World fleet (July 2022)

The new construction and the S&P market as well as the charter and the freight markets are main drivers of shipping markets supplying vessels to transport of seaborne cargo. The secondhand ship market condition fluctuates relating primarily with freight rates, and the volatility more amplifies when the freight rate interact with market sentiment. Stopford(2009) investigates how the dry cargo shipping cycles have behaved over a 266-year period, between 1741 and 2007, and identifies 22 prominent shipping cycles lasting 10.4 years on average over the centuries. If a shipowner or an investor is capable to prospect the future market trends and ride on the favorable shipping business cycle, then they will be in the advantageous position than the other competitors when determining direction either invest or sell out an asset. However, since the shipping business is a cyclical and highly volatile market that is affected by a variety of tangible and intangible factors, it is not a market that circulates with certain rules that investors adopt as a standard and use it as a kind of rule of thumb, so it is impossible to predict that past records will similarly occur in the present or future markets. Therefore, an investor will require an insight in respect of market dynamics before investment so that they can achieve the better commercial outcomes. Depended on the visibility of future market horizons, the strategy of investors, banks and even regulators will pursue differently. Because of this unpredictable volatility, the supply of shipping finance from government financial institutions as well as commercial banks tend to reduce shipping capitals typically from Europe traditional shipping finance banks since global finance crisis in 2008. Even though such a recent adverse and compressed shipping market circumstance, the data produced by Clarksons Research on a weekly basis from January 2018 to July 2022 based on their own records and from data they have collected from third parties appears that there were 8038 cases of sale & purchase activities. The ASIASIS(2022) also reports that there were transactions amounting about 43 billion USD in 2021 which is 53% year on year growth against 2020 and ever record within recent 10 years in the S&P market.

This study focuses the weighting of the factors that determine the price of secondhand Bulk carriers and Oil tankers, and it expands the scope further down to sub-segmented sizes of each ship type. The design of this research model is based on the S&P data of secondhand ship transactions of the last four years, January 2018 – April 2022, for various types and sizes representing for Bulk carriers and Oil tankers. The independent variables are selected from not only conventional asset value, macroeconomic relating variables and country of new construction(Dummy variable) but also an industrial production index that have been rarely applied in the previous studies to verify the correlation with the secondhand ship prices through regression analysis so that this study approaches determinants at wider spectrum. This study will serve as a reference for investors who is looking for feasibility of investment in the secondhand ship market by verifying the causality with multiple variables and ship sizes from the latest secondhand ship S&P trading data through empirical analysis.

The structure of the study is as follows. Section 2 review previous literatures on the various determinants impacting secondhand ship prices. Section 3 presents the research design used in the study to investigate the determinants-price relationship in the secondhand ship markets. Section 4 presents the empirical analysis and discussion, and section 5 presents implications of findings and conclusions.

2. Literature Review

The demand side of shipping market which is seaborne trade is being continuously increased. The global economy and seaborne trade are experienced a firm rebound from the impacts of COVID-19 and seaborne trade is now recovered at pre-pandemic levels(Clarksons Research, 2021). According to Clarksons Research(2022), the maritime trade volume was 12,093 million tons in 2021, which is similar with the 2019 trade volume of 12,121 million tons. Stakeholders relating shipping market takes great interest in the freight rates. The freight transport cost will fluctuate significantly along with volume of demand to transport the seaborne cargo and volume of supply to be able to carry the cargo. If backlog cargo is drastically increased and a shipper gets impatient in the potential delaying of cargo booking, the freight rate at the peak season tends to sharply hike. Kim(2022) studies diverse variables impacting to the freight rate, and it finds that Clarksea index is impacted by the Brent oil price and world seaborne trades, and Clarksons average bulk earnings is only impacted by world seaborne bulk trade while Clarksons average tanker earnings is impacted by world seaborne oil trade, Brent oil price, industrial production OECD and inflation. The freight rates of major shipping segments is being periodically published through the indices of major seaborne cargo segments such as the Baltic dirty and clean indices for Tanker market, the time charter rate and spot freight rates for the Containers market, and BDI(Baltic Dry Index) including BCI(Baltic Cape Index), BPI(Baltic Panama Index), BSI(Baltic Supramax Index) and BHI(Baltic Handysize Index) for Bulk carrier market. The Clarksea index is the timeseries tracts averaging vessel earnings across the Tanker, Bulk carrier, Container, and Gas carrier weighted by the number of ships in each segment.

The shipping market is another market which is applicable for ‘economies of scale’ theory by increasing ship’s size to reduce a transport unit cost of a cargo. There are diverse types and sizes of ships are operating to carry a different cargo and parcel size. The ship size has been experiencing gradually increased to keep the seaborne freight cost remains competitive in the transportation market. In other words, the shipping market is being much segmented according to the type of cargo, and the ship’s sizes are also being increased particularly for long-haul cargo, and in the Container segment and Ore carrier segment(Stopford 2009). The fatigue life of the vessel is in general about 20 to 30 years after delivery from the new construction shipyard. The vessel delivered from the new construction shipyard equips a brand-new design and technology, however, whilst performing transporting services over the years, the ship become aged, system get obsoleted and operating cost including maintenance cost is gradually increased resulting uncompetitive in the market. For a variety of business reasons, a ship owner may want to sell a vessel to an investor who wants to make a profit from the purchase of a vessel in the S&P market, with the intention that the ship owner will see a future slowdown in the freight market or to restructure their fleet portfolio or to improve a healthy balance sheet in their financial account(Stopford, 2009). This attempt creates the secondhand ship market.

The secondhand ship price will be adjusted depending on the severity of freight rate and investor’s sentiment as well as level of imbalance of demand(seaborne trades) and supply(world fleet volume) market resources. There have been various previous studies about factors constituting in the secondhand ship prices for long period. This empirical study particularly singles seven variables out impacting significantly to the secondhand ship prices from those known factors through the previous literatures. This empirical analysis utilizes ship’s size, age, Clarksons average bulker/tanker earnings, LIBOR, inflation indicator OECD and industrial production OECD to examine an impact of those independent variables determining the value of the secondhand Bulk carriers and Oil tankers. Haralambides et al.(2005) approaches the factors impacting determining the prices of new construction ships and secondhand ships through economic theory bases which is rarely attempted in the previous studies. This study finds that the new construction price and time charter rate have a significant causal relation with all variables determining of secondhand Bulk carrier and Oil tanker prices. In respect of capital cost is significant only for the Bulk carrier shipowners, and order book ratio has a negative relation with Panamax, Suezmax and VLCC Tankers. This study concludes that the secondhand ship prices are primary market driven whereas new construction prices are mainly for cost driven as well as Bulk carrier is more cost driven than revenue driven. In this point, if capital cost is significant for Bulk carrier shipowners, then there is some potentially open questions about when will be the best time to invest to the bulk carrier market to match up with such result.

The volatility of the secondhand ship prices in the S&P market is heavily related with the ship’s size. Kim et al.(2014) tests dynamic relationship between bulk freight indices and secondhand ship prices with application of the size and age factors of the Bulk carriers using Vector Autoregressive(VAR) Model. The study analyzes the relationship between the secondhand ship prices of Panamax and Cape bulk carriers at the age of 5 and 10 years and the BDI, BCI, BPI indices collected over 15 years period of monthly time series data. The result appears that the freight indices impacts the secondhand ship prices whereas the secondhand ship price does not impact on the freight indices. Furthermore, the price volatility is more severe on younger ship and bigger sized ship than aged ship and small sized ship. One of the interesting question in this context is that this finding somewhat disaccords with a common belief that increment of secondhand ship price will be concomitant with increment of freight rate. Yang(2017) argues that the market price of a secondhand ship may be undervalued when the economy is recessed, if the ship’s price is simply determined by market price. Therefore, to define fair value of a ship, Yang suggests the Hedonic Price Model(HPM) which is applicable for diverse physical variables characterizing actual ship’s performances. The Regression Analysis through the Log-Liner semi-log function model concludes that the age, market value, shipbuilder, DWT, short term & long term charter rates, en-bloc and special survey due influence the ship secondhand ship prices whereas OPEX, Light Displacement Weight(LDT) and bank sale don’t. This report implies an importance of fair value evaluation model so that the ship’s price does not distort.

There are some attempts to compare analytical performance between conventional Multiple Regression Model(MR) and Artificial Neural Network(ANN) Model trials. This study often finds that the ANN Model demonstrates its superiority than the result taken from MR Model. Park et al.(2022) carries out an experimental study to develop the forecasting model of secondhand Cape bulk carrier prices using ANN Model incorporating market factor variables, macroeconomic variables and BCI variable. From the correlation analysis, the prices of the secondhand Cape bulk carriers show positive correlation with order book, bunker price, CIPI(China Industrial Production Index), interests and BCI. This study result shows contrary against the other study which argues that order book has a negative correlation with secondhand ship price. This unexpected finding signals the need for additional studies to understand more about these causalities. The comparison of performance of developed ANN Model and MR Model finds superiority of ANN Model, and consequently suggests active utilization of ANN Model. Lim et al.(2019) also proposes the superiority of performance of the ANN Model against the Stepwise Regression Analysis Model. It views that the secondhand ship market is important in the shipping market because it offer an investor to be able to enter the market readily whereas new construction market takes time lags for a few years until deploy the vessel to the market. However, before entry to the market, an investor is to acquaint with configuration of the secondhand ship prices so that the investor will sit in the better position in the financial terms by reducing capital cost. The study adopts three effective variables out of 6 determinants being taken from the previous literatures which are freight rates, ship’s age and size, and subsequently carry out performance test of those key parameters using 10 folds cross validation method of ANN Model. The study finds more reliability of ANN Model. Even though there is evidence of superiorities of ANN Model in the previous studies, this empirical study applies the Multiple Regression Model which was conventionally used for the similar studies. In the case of Alizadeh and Nomikos(2003) applies the relationship between prices and trading activity as the variables determining the price in the secondhand Bulk carrier market, and find that price change induces more transactions but increased transaction volume leads to a negative influence to the volatility of price changes. This study also appears that high capital profit helps invigoration of secondhand S&P market and consequently contribute to the market stability by mitigating volatility.

No doubt, the new building market is led by South Korea, Japan, and China by sharing of above 80% market share, and each country is keen to improve their own competitiveness to cope in the strong market competition. The competitiveness of each country is consequently reflected in the secondhand ship S&P market by transaction of differentiated ship prices. Hwang and Park(2018) study the competitiveness of those three global leading new construction countries. Chinese’s new construction market is known for labor-intensive strategy to outperform their competitors, and this strategy appears well work since global financial crisis of 2008. Contrarily, Japan and South Korea markets pursue the technology-intensive strategy with stepping into global industry pathway and IMO environmental regulations. Empirical study using three dimensional Lokka-Volterra model proves that although China positions an advantage than Japan and Korea by maximizing their labor-intensive strategy for a while, however China may lose competitiveness in near future unless they proactively adopt the technology-intensive strategy. Lee(2019) measures the shipbuilding competitiveness of China and Korea. Lee carries out empirical study with new construction technology, new construction price and export credit variables. The study finds that the China is dominant position than Korea in terms of the new construction contract price and the export credit particularly in the standard Bulker and Container segments. Korea keeps its competitiveness only in LNG segment with supportive of strong new construction technologies. The study views that the global new construction industry leadership will be moved to China soon provided China improve market power by developing of technologies and credibility of shipowner under the circumstance of cheap labor cost. In fact, China’s new construction competitiveness is increasing, and it can be seen that it has sufficient competitiveness for the most of ship types except LNG carrier, ULCS(Ultra Large Container Ship) or VLCC, which require relatively high construction prices and technologies.

Literatures for secondhand ship price determinants

3. Research Design

3.1 Sample

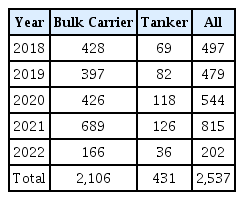

The sample of this study is based on S&P performance, and macroeconomic indicators in the secondhand ship market for Bulk carriers and Oil tankers provided by Clarksons Research. The study uses S&P transaction data from January 2018 to April 2022, because the study is interested to research the current secondhand market phenomenon. The data is the latest one with sufficient samples and accuracy covering all variables singled out for this study. In addition, the study was also intending to analyze the relationship with COVID-19 although it was removed from the variable due to significant multicollinearity against macroeconomic variables. In the case of macroeconomic indicators, the data set is completed by matching monthly data based on the trading day of each secondhand ship. After data cleansing by removal of numerous missing data and outlier, there are total of 2,537 secondhand Bulk carriers and Oil tankers’ sales data, 2,106 Bulk carriers and 431 Oil tankers, are extracted as a valued sample. The samples are sub-segmented in accordance with vessel size as Hanymax including Handy size(25,000∼ 49,999 DWT), Panamax(55,000∼110,500 DWT) and Cape (110,501∼209,999 DWT) for Bulk carriers, and Afamax (85,000∼119,999 DWT) and VLCC(200,000∼325,000 DWT) for Oil tankers. The sub-segment of Bulk carrier and Oil tanker segments used in this analysis are categorized in accordance with Worldyards’ segment definition(2003). Details of the sample are shown in the Table 3.

S&P of secondhand ships

3.2 Variables and Analysis Methods

In this study, using Multiple Regression Analysis, we intend to investigate the influencing factors affecting the price determination of secondhand ships. This is to analyze whether the independent variables selected through previous studies having significant effect on the dependent variable which is the secondhand ship price. First, empirical analysis is carried out on 2,537 samples of all ship types, and analysis was performed by dividing Bulk carriers and Oil tankers. In the analysis by ship type, additional analysis is performed to find out whether the variables affecting the sale price which is a dependent variable differ according to the size of the ship. The Multiple Regression Model for this study is as follows.

Here, Ŷ is sale price of vessels, X1 is size of vessels, X2 is age of vessels, X3 is ClarkSea Index as a freight rate, X4 is US$ LIBOR 6 Months, X5 is inflation indicator OECD, X6 is industrial production OECD, X7 is building country dummy(Japan=1) and X8 is also building country dummy(Korea=1).

4. Empirical Analysis Results

4.1 All Vessels

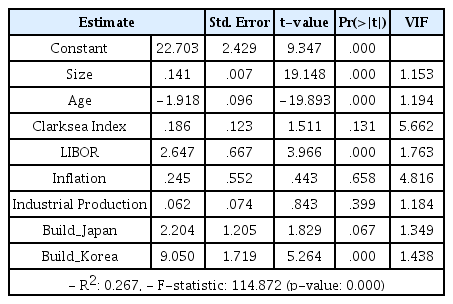

The Table 5 shows the analysis result of the secondhand ship pricing model for all ship types.

Result of regression (All samples)

The size, age, LIBOR, and building country (Korea) are found to have the significant effect on the secondhand ship price, which is the dependent variable, at the 95% confidence level. Size and LIBOR have a positive effect on secondhand ship price, and age has a negative effect. The secondhand ship price built in Korea appears higher than those built in the other countries. At the 90% confidence level, the secondhand price of ships built in Japan is also higher than that of ships built in the other countries except Korea.

4.2 Bulk Carriers

Table 6 is the analysis result of the secondhand ship pricing model for Bulk carriers.

Result of regression (Bulk carriers by ship size)

For Bulk carriers, the entire Bulk carriers are analyzed, and it is further analyzed by sub-segmented ship sizes. Analysis of all Bulk carriers show that Size, Age, Clarksons average bulker earnings, LIBOR, and Inflation indicator OECD show the significant effect on the secondhand ship prices at the 95% confidence level. All significant variables except age appear to have a positive effect on the secondhand ship price. In the case of building country, at the significance level of 90%, the price of secondhand ship built in Korea appears higher than those of ships built in the other countries. In the case of Handymax, it is found that size, age, Clarksons average bulker earnings, LIBOR, and inflation indicator OECD show the significant effect at the 95% confidence level. All significant variables except age appear to have a positive effect on the secondhand ship price. However, in the case of the building country variable, it does not appear to affect the dependent variable. For Panamax case, size, age, Clarksons average bulker earnings, LIBOR, and inflation indicator OECD show the significant effect at the 90% or 95% confidence level. In the case of the building country, the secondhand price of ships built in Japan appears higher than that of ships built in the other countries at the 90% confidence level. Finally, the analysis result of the Cape bulk shows that age, LIBOR, and inflation indicator OECD have the significant effect on secondhand ship price at the 90% or 95% confidence level. The price of secondhand Cape bulk built in Korea also appears higher than that of ships built in the other countries at the 90% confidence level.

4.3 Oil tankers

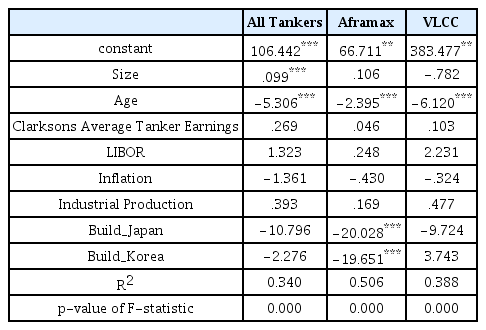

Table 7 is the analysis result of the secondhand ship pricing model for Oil tankers.

Result of regression (Oil tankers by ship size)

Analysis of all Oil tankers show that size and age variables are found to have the significant effect on the secondhand ship prices at the 95% confidence level. Next, a result of analysis for the Aframax is shown that age and building country variables are found to have the significant effect on the secondhand ship price at the 95% confidence level. In the case of building country, it is analyzed that the secondhand ship price built in Korea and Japan are transacting at significantly lower price than ships built in the other countries. This unexpected finding signals the need for additional studies to understand more about the building country variables. Finally, the analysis result of the secondhand ship pricing model for the VLCC shows that only age is the variable having a significant effect on the secondhand ship price at the 95% confidence level.

5. Conclusion

This paper examines the factors determining the prices of the secondhand Bulk carriers and Oil tankers using the Multiple Regression Analysis. The samples taken from the S&P data transacted in between Jan 2018 and Apr 2022, and variety of independent variables are adopted to research relationship with the recent S&P transactions. The results of this empirical analysis appear that: Firstly, in the secondhand ship pricing model for the entire segments, age, LIBOR, and building country show a significant impact on the price of secondhand ship. Secondly, the analysis for Bulk carriers shows that size, age, Clarksons average bulker earnings, LIBOR, and inflation indicator OECD are variables that affect the price of secondhand ship. It is also found that the Panamax bulk carrier constructed in Japan and the Cape bulk carrier constructed in Korea appear transacting with higher prices than those vessels constructed in the other countries. The reason is that the competitiveness of shipbuilding in both countries seem to have gained differential advantage in the market over the past decades due to technological superiority, reduced construction time and continuous delivery of high-quality ships. In Oil tanker’s case, on the other hand, almost all the ships traded on the S&P market were built in Korea or Japan, which showed somewhat different results in the empirical study, which seems to be a proposition to be clarified in future studies. Thirdly, in the case of Oil tanker, unlike bulk carriers, only the size and age variables are selected as independent variables that affect the secondhand ship price. In the case of Aframax tanker and VLCC, the age and building country variables for Aframax and only age variable for VLCC is found to have the significant effect on the price.

Through this study, we enable not only identifying and weighting the impact of each independent variable on the secondhand ships being transacted in the S&P market, but also finding somewhat different trend in the determinants depending on ship types and ship sizes. In the case of age, by showing significant results in a negative direction, regardless of the type and the size of the vessel, influence of age is considered by investors to be the most common and important factor in determining secondhand ship prices. The variables other than ship size and age are found significantly related to ship type and size. In the case of the industrial production index is none of relation with secondhand ship prices. The other macroeconomic variables also do not affect the pricing of secondhand ship except for bulk carriers, which contribute to the reaffirmation of the previous research that the secondhand ship market is primarily market-driven. This paper argues that when an investor decides to invest in the secondhand ship market, it is necessary to consider the weight and type of the secondhand ship price determinants as well as the market situation of the secondhand ship market as a whole. This study is meaningful in that it empirically analyzes the secondhand ship pricing model using Bulk carriers and Oil tankers, which are the most recently transacted in the secondhand ship S&P market. This report expects to expand the scope of investors’ practical applications by applying statistical verification of factors influencing secondhand ship price estimation to various classes of Bulk carriers and Oil tankers. The difference of this study is that macroeconomic indicators and new construction countries are used as independent variables for the determining of secondhand ship pricing of diverse sizes of Bulk carriers and Oil tankers. It is also hoped that future research will not be limited to these two ship types but will be able to extend its scope to the other major ship types such as Containers and Gas carriers who are being heavily recognized in the recent shipping market.