1. Introduction

With the integration of global economy, the emergence of Asia-Pacific countries is a major unfolding phenomenon. This is especially compelling in the maritime spectrum. According to the United Nations Conference on Trade and Development (UNCTAD, 2020), for example, seaports in the Asian region handled 527 million TEUs in 2019, which is equivalent to 64.9% of world total container port throughput. Moreover, among the leading 20 container ports, 15 seaports are located in Asia. In this regard, as a growing number of global companies are keen to secure international logistics centers in East Asia, the competition between major economies in this region (China, Japan and South Korea) to attract them in the port hinterland is ever escalating (Kang and Kim, 2015).

Although the East Asia region leads the global shipping market in terms of physical infrastructure (for example, shipping operation, shipbuilding and port logistics), it is widely accepted that relevant services, such as finance, insurance, broking and information, are far behind when compared to other regionsŌĆÖ maritime clusters, such as London, Singapore or New York. Especially, financial service is instrumental in developing the shipping industry. Notably, given the fact that shipping investment requires a considerable amount of initial capital for a long project life, the survival of a shipping company largely depends on its ability to secure funding at a low capital cost (Stopford, 2008). In addition, financial liquidity and risk management play a key role in running shipping business under the excess volatility, cyclicality and seasonality of freight rates and shipping assets (Kavussanos et al., 2021). Therefore, one of the recently emerging agendas in the East Asian region is supporting the shipping industry through the establishment of the maritime financial center.

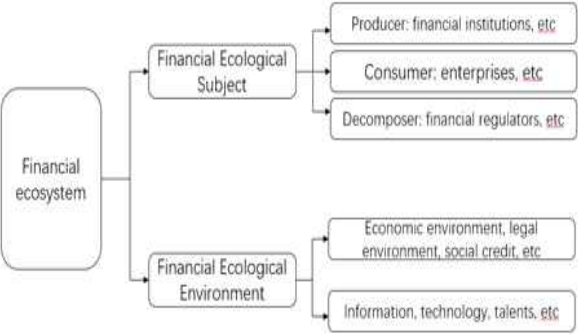

In this regard, this paper aims to construct an evaluation index of maritime financial centers in terms of financial ecological environment. The concept of the financial ecology was first proposed by Xiaochuan Zhou, the former Governor of the PeopleŌĆÖs Bank of China, in 2004.1) The financial ecology is a bionic concept formed by the integration of the ecological theory from natural science and the financial theory from social science. Accordingly, the basic content of the financial ecology includes stable economic environment, sophisticated legal environment, good credit environment, coordinated market environment and other factors (Zhang et al., 2006). The main idea is that the financial ecosystem can work well when the ecological subjects (financial institutions, financial markets, regulators and consumers) and related environment paly their own characteristics and functions (see Fig. 1). Therefore, the concept of financial ecology has constructed a new research framework for the interactions between financial market participants and relevant circumstances.

Based on the evaluation index, this paper examines the shipping finance environment of Qingdao, the economic hub of Shandong Province, as a numerical example. Located in the eastern end of China, Qingdao is a major seaport in the Northeast Asian region with the container throughput of approximately 20 million TEUs in 2019 (UNCTAD, 2020). Along these lines, the cityŌĆÖs financial services for the shipping industry has also been improved. For instance, QingdaoŌĆÖs ranking in Global Financial Centers Index has jumped up to 29th in 2019 from 79th in 2016. In addition, corporate income from cargo transportation insurance premium in Qingdao has more than doubled for the period between 2010 and 2019.2) Moreover, this study also performs a longitudinal comparison with Shanghai and discusses what can be the measures to improve the shipping financial ecological environment in Qingdao as a fast-follower.

By doing so, this study can contribute to the related literature in two ways. First, the findings in the paper can provide some important implications for maritime financial center policy of Busan. Despite the KoreaŌĆÖs global competitiveness in the shipping, port and shipbuilding sectors, it is widely perceived that the maritime finance of Korea is still in a fledgling stage. (Kim et al., 2016). In stark contrast, Japan has a long history of shipping finance practice based on the relationship banking, for example, Ehime Senshu in Imabari Maritime Cluster (Han, 2018), while a number of Chinese financial institutions have rapidly increased their exposure to the shipping sector (Kim, 2019). Against this background, while there has been a great deal of effort to establish the global presence of Busan as a maritime financial cluster since 2009, the results are, by and large, away from being a success thus far (Kim and Park, 2016). Therefore, the findings in this study can bridge the gaps between policy goals and practical initiation. Second, while previous studies addressing the shipping finance center in Korea offer several constructive suggestions, such as improved transparency in corporate governance of shipping companies (Kang, 2017), diversification of funding sources, promoting the participation of commercial banks (Kim, 2019), constructing cluster of financial institutions (Cho and Lee, 2011; Kim et al., 2016) and establishing a control tower for policy coordination (Kim and Park, 2016), the vast majority of them are based on limited number of observations or qualitative discussion, rather than quantitative analysis. Therefore, significance of this study lies in suggesting a new quantitative approach for research on the subject of maritime financial centers.

The rest of this paper is structured as following: Section 2 reviews previous literature addressing financial ecological environment. Section 3 describes the dataset and the methodology employed in this study. Section 4 provides analysis results. Finally, Section 5 concludes this study.

2. Literature review

Since the concept of the financial ecology was highlighted by Xiaochuan Zhou in 2004, there has been a considerable amount of research providing empirical evidence on the impact of financial ecological environment mainly driven by Chinese researchers. Yang and Yu (2020) investigate the association between the construction of financial ecological environment and the growth of small and medium-sized enterprises (SMEs). They find that the favorable financial ecology relieves financial constraints of SMEs, which leads to their growth. Huang and Zhang (2020) document a similar observation for the positive impact of financial ecological environment on the investment efficiency of SMEs listed on the Shenzhen Stock Exchange. In addition, there are several studies that examine the financial ecological environment in regional provinces for Hebei (Wang et al., 2020), Inner Mongolia (Yang and Zhang, 2020) and three northeastern provinces of Liaoning/Jilin/Heilongjiang (Zhang and Ma, 2020).

Furthermore, a strand of research highlights the financial ecological environment centered on the shipping industry. Zhu and Zhao (2012) provide the theoretical basis of the construction of the shipping financial ecological environment in China. Chang (2017) analyzes the characteristics of the global shipping finance market and points out some challenges in the development of ChinaŌĆÖs domestic market. Zhang and Sun (2018) compare the development status and the business environment of leading maritime centers, suggesting that enhancing shipping finance environment can lead to the establishment of an international shipping cluster. Moreover, some other researchers focus on the construction and the evaluation of the shipping financial ecological environment on the regional level, such as Shanghai (Wang, 2015; Zhong, 2019) and Guangzhou (Zhang, 2018).

Despite a plethora of studies investigating the factors for improving the shipping financial ecological environment in China, little research attention has been paid to the current status of shipping finance in the under-developed regions such as Qingdao, Tianjin and Ningbo. Although those regions are rapidly growing in terms of shipping transport and seaport throughput, relevant financial service is still in poor condition. Therefore, it is of utmost importance to examine the development status of fast-growing ports in terms of shipping finance environment and to suggest the ways to enhance shipping finance service.

3. Methodology and Data Description

In order to assess the shipping financial ecological environment, this paper employs the fuzzy comprehensive evaluation (FCE) based on the entropy value method. The entropy value method is a mathematical function used to judge the degree of dispersion of an index. The FCE is a combination of qualitative and quantitative decision-making process to make comprehensive judgments by considering a variety of factors Zhang and Yang, 2012). The greater the degree of dispersion, the greater the influence of the index on comprehensive evaluation. According to ShannonŌĆÖs information theory (1948), the level of information entropy carried by an index is positively associated with the disorder degree of information, which also indicates that the effectiveness of the information carried by the index is positively associated with the weight of the index. In the entropy value method, the weight of an index is determined as:

where wi is the weight of the index j, gi is the difference degree of the index j in different years derived from the entropy value of 1 - ( - 1 ln m ├Ś Ōłæ i = 1 m p i j ln p i j )

The FEC is based on the fuzzy set theory of Zadeh (1965) for identifying the uncertainties and dynamics in information. The first step of FEC is the establishment of a single factor comprehensive evaluation matrix as following:

where rij is the degree of the element i in the set of evaluation indices (U) and the element j in the set of evaluation grade (V).

Then, the total score of the evaluation object (F) is calculated as:

where W is the index weight vector obtained from the entropy value method, R is the comprehensive evaluation matrix and S is the score of the corresponding evaluation grade.

Based on the previous literature, the dataset for shipping ecological environment in Qingdao is collected from Win.d, a Chinese financial data service provider, and the evaluation index system is examined in five critical layers: (1) Basis of shipping economy, (2) Shipping financial development, (3) Credit environment, (4) Legal environment and (5) Governmental behavior. Each critical factor includes sub-criteria in the index sign layer as shown in Table 1. In addition, Table 2 shows the descriptive statistics for each index sign layer variable for the period between 2010 and 2019.

4. Analysis Results

Table 3 presents the weights of indices for shipping financial ecological environment calculated by the entropy value method. For the level of Criteria Layer, the basis of shipping economy is found to be the most important factor with the weight of 0.4022, followed by governmental behavior (weight of 0.2273), shipping financial development (weight of 0.1786), credit environment (weight of 0.1433) and legal environment (weight of 0.0485). Among the four sub-criteria of the basis of shipping economy, the weight of fixed assets investment in the shipping industry is the highest with the weight reading at 0.4137.

Based on the above index weight, the scores for criteria layer variables as well as the comprehensive shipping financial ecological environment are calculated by the Equation (3) and the results are presented in Table 4

Generally, it appears that the shipping financial ecological environment in Qingdao shows a downward trend (see Column (1) in Table 4). The assessment score has decreased from 79.1 in 2010 to 67 in 2019 despite some exceptions of increase in 2011, 2014 and 2015. The main driver of the deterioration in QingdaoŌĆÖs shipping financial ecological environment is the basis of shipping economy. Specifically, the correlation coefficient between the shipping financial ecological environment and the basis of shipping economy is 0.9136. While other indices also have a downward trend, the legal environment and the governmental behavior have shown a stable recovery since 2016.

Finally, this study compares the shipping financial ecological environment in Qingdao with that in Shanghai, the leading economic area in China. While the indices for Shanghai are calculated in the same way as Qingdao, the comparison is performed only for the period of 2014-2018 due to data unavailability. The results are shown in Table 5. It is quite evident that the gap between Qingdao and Shanghai in terms of the shipping financial ecological environment has widened for the period of 2014-2018. While the shipping finance environment in Qingdao has been stagnant, that in Shanghai has increased from 74.6 in 2014 to 99.4 in 2018 (see row (1) in Table 5). The same phenomenon of widening gap between Qingdao and Shanghai is also observed in the basis of shipping economy, shipping financial development, credit environment and governmental behavior. The only exception is found in the legal environment in which both cities show improvement.

5. Conclusions

This paper examines a new evaluation index for the development of the maritime financial center in terms of financial ecological environment. For this purpose, this study constructs an index of the ecological environment of shipping finance based on five criteria: the basis of shipping economy, shipping financial development, credit environment, legal environment and governmental behavior. In addition, the development of shipping finance environment in Qingdao for the period of 2010-2019 is analyzed by employing 11 sub-indices and the results are compared with that of Shanghai. It is found that the shipping finance environment in Qingdao has deteriorated for the past decade and the city needs to support its local maritime and the financial industries to establish its presence as a maritime financial center.

The findings in this paper provide valuable contributions and implications for the maritime financial policy of Busan. First, as the financial ecology theory suggests, it is critical to establish harmonious environment fostering both shipping and financial industries. Second, constructing a reliable shipping finance environment index is highly recommended for better understanding the current status of Busan and comparison with other competiting cities. Finally, relevant to the second point, it is of paramount importance to indentify the strength and weakness of Busan as a potential maritime financial center and to implement effective policies.

Despite the important findings in this paper, there are some unfilled gaps that deserve research attention in the future. Among them, it should be noted that there are some possible alternatives for sub-indices in the index sign layer. Specifically, for the degree of shipping finance development, this study examines only insurance premium for ship and cargo due to data availability. However, there are a plethora of other indices that can reflect shipping finance development, such as the amounts of equity capital raised via stock market, shipping high-yield bond issues, ship funds and leasing, to name a few. Therefore, future research can provide more valuable insight by expanding the kinds of sub-indices.

PDF Links

PDF Links PubReader

PubReader ePub Link

ePub Link Full text via DOI

Full text via DOI Download Citation

Download Citation Print

Print